What

is a real economic good?

Simply put, a real economic good is anything that is naturally scarce and in demand. Scarcity implies that you cannot get all of the good that you want freely from nature and there is nothing anyone can do to change that, therefore someone must employ resources and produce it and you must pay for it.

For example, on a sunny Floridian day you can get all the sunshine you want for free by just going outside. Someone doesn’t have to produce sunshine and you don’t have to pay anyone for it. On the other hand, you cannot get all the sun protection lotion you want freely from nature, someone must produce it and you must pay them for it. Therefore, sun lotion is a real economic good. The supply of a real economic good is determined in the market as a function of demand and price.

What is an artificial economic good?

An artificial economic good is a good that is artificially scarce. For example, sunshine on a sunny Floridian day is not scarce, but if someone is locked in a basement with a single window that is controlled by someone else, then sunshine becomes scarce for the basement dweller. If he wants sunshine he must pay someone to open the window and let the sun in.

In other words, a real economic good is a good that is scarce by its nature and always will be regardless of the influence of any outside forces. An artificial good is a good that is not scarce by its nature but because of the influence of outside forces. The supply of an artificial economic good is not determined in the market as a function of demand and price but rather by forces outside the market such as a central committee, a governing board or business rules in a software program. Therefore, supply is unaffected, completely insensitive to market forces.

What is a Bitcoin?

In realty a Bitcoin is nothing more than a text string in a text file that is part of a blockchain. A blockchain is a collection of text files that are related to and mathematically dependent upon one another in an attempt to initially solve the double expenditure problem of digital money.

By its nature, there’s no reason why a computer program couldn’t be written to create text string entries in a text file in a blockchain without end. It’s just a text string so the code could be written to produce bitcoins non-stop ad infinitum, there are no natural barriers to this. Text strings in text files are not scarce by their nature. The only way to prevent that from happening is by choosing to implement constraints in the code to make the supply of Bitcoins artificially scarce by using programmatic forces to influence how many Bitcoins are produced and when. Therefore, Bitcoin is an artificial economic good which is not scarce by its nature but artificially scarce by design. The supply of Bitcoin is not determined in the market by market forces but by business rules in the code and is therefore completely insensitive to changes in demand and price, perfectly inelastic.

As of today, 6.25 new Bitcoins are created every 10 minutes according to the business rules in the code controlling the supply of Bitcoin. But the programmers who wrote the code could have made that anything they wanted. They could have made it a million Bitcoins per minute or 10-100 Bitcoin per year. The decisions they made for influencing the supply of Bitcoin were arbitrary and meaningless, a centrally planned artificial economic good.

A Bitcoin is a perfectly complementary artificial good with no substitutes

The Bitcoin blockchain is a payment network and a Bitcoin is a perfectly complementary artificial good to the Bitcoin blockchain. In the same sense that a lamp is of no use as a source of light without a lightbulb, you can’t make payments using the Bitcoin payment network without having Bitcoins. But a lamp is a real economic good and can have alternative forms of utility like being used decoratively so light bulbs are not necessarily needed for a consumer to value a lamp. Contrarily, the Bitcoin payment network requires the consumer has Bitcoins and only Bitcoins in order to use it, it is useless without them and there are no alternative uses for it. You can’t send dollars or gold or anything else on the Bitcoin blockchain, only Bitcoins, Bitcoins have no substitutes.

It’s important to make the distinction between what one uses in trade to buy things and how they pay for those things. A blockchain and the entries in it called Bitcoins comprise the Bitcoin payment network. The Bitcoin payment network is a transaction medium that accounts for transactions between users but the price negotiation is always in fiat because goods are valued and priced in fiat, nothing is valued or priced in Bitcoin. Once the price is agreed on, the equivalent in Bitcoin at the moment is calculated and the buyer creates a transaction to the seller on the Bitcoin blockchain for the fiat equivalent of Bitcoins. Fiat was used in trade and the Bitcoin payment network is what is used to pay or send the value of the fiat to the seller. Bitcoins are used as a proxy or token that represent fiat value in order to account for the transaction on the Bitcoin blockchain.

Key point: A payment medium is not the same thing as a medium of exchange.

What is a real medium of exchange?

First and foremost a real medium of exchange is a real economic good which eliminates Bitcoin immediately. Secondly, it’s a good that has emerged from the market a priori as a durable, highly saleable good due to its utility and value across markets. In other words producers and consumers have confidence that its physical nature will resist time and that it will be accepted in trade because it has a history of being traded for its utility and value across markets. Only then is it adopted as a standard measure of value across markets and a medium of exchange. If a good is easily destructible and/or has no history of its saleability across markets, then it won’t emerge from the market as a medium of exchange. Put another way: a real medium of exchange, a real standard measure of value cannot be declared by a central authority, it’s a naturally occurring market emergence phenomenon in which a durable good had utility and value across markets first, only then it emerged as a medium of exchange because of that durability and market utility.

Bitcoin has no utility except as a complementary good to the Bitcoin blockchain which appeared at the same time as Bitcoin. It has no history before the blockchain, it never had utility or value across markets because you can’t take a Bitcoin off the blockchain and use it for anything else.

A real medium of exchange serves as a standard measure of value which means that other goods are priced in terms of it. Nothing is priced in terms of Bitcoin because nothing is valued in terms of Bitcoin. All goods are valued and priced in terms of fiat. When someone agrees to pay using the Bitcoin payment network, the price is quoted in fiat and then converted to the equivalent amount of Bitcoin at that moment. The Bitcoin and the blockchain are the physical vehicle used to account for the transaction but the value of the sale was calculated and paid in fiat.

Opportunity Cost

Investors speculate on all kinds of real goods like gold, silver, land etc. But there's an opportunity cost associated with holding real goods for speculative purposes. If you buy land, for example, and just hold it hoping the price goes up, rather than farming it, leasing it out or developing it, then you are losing the potential profits from those alternative opportunities. You're hoping the price goes up enough so you can sell it to cover those opportunity costs plus some profit margin.

That's not the case with Bitcoin, you either use it to pay for something on the Bitcoin blockchain or you don't, that's it. And if you don't use it on the Bitcoin blockchain then you are holding it and you can sell it any time you want. Of course you want to sell it for at least what you paid if not more so you'll wait for the price to be right. When you buy something, hold it and then sell it at a later date for profit if possible, that's speculation whether that was the intention or not.

In other words, by its nature there are only two things you can do with a Bitcoin: use it on the blockchain or speculate with it and if you’re not using it on the blockchain you are speculating.

Key point: This “unintentional” speculative demand is therefore an innate characteristic of Bitcoin.

What is a store of value?

Whether a good is a store of value or not depends on its economic fundamentals since storing value is a long-run phenomenon. The short-run price of a store of value will vary but its fundamentals will ensure that it has value in the long-run that can be used in exchange whatever that value might be at the time.

Key point: a store of value doesn’t mean a high price in the long-run, it means that the good will have value that can be exchanged in the long-run regardless what the price is.

A store of value has to be durable so that regardless what happens to it physically, the nature of the good is difficult for the consumer to destroy so it can be used in exchange in the long-run. An ice cream cone doesn’t make a good store of value since the ice cream will melt and all you’ll be left with is the cone. But since gold and silver are fundamental elements, regardless what form or state they are in, they’re still gold and silver. That’s true for any precious metal so precious metals are durable.

A store of value has to have utility and value across markets so that even if it loses value in one market, it still has value that can be exchanged in others. This diversity of value is what insures that the good will be valued in the long-run. Although a bowling ball is durable and difficult for the consumer to destroy its value is limited to the context of bowling and doesn’t have diverse value in other markets. The long-run value of a bowling ball depends on the demand for bowling and bowling alone. If the demand for bowling dries up so does the value of bowling balls so bowling balls don’t make a good store of value.

Gold, silver and other precious metals are durable and have utility and value in a large number of markets: adorning furniture, adorning clothing, jewelry, electrical circuits, heat shielding etc. Precious metals have the sort of durability and market diversity that makes them a good store of value that can be exchanged in the long-run.

Is a Bitcoin a store of value?

Is a Bitcoin durable, is it difficult for the consumer to destroy the nature of it? Kind of an odd question for a text string in a text file but the answer is no. If you keep your Bitcoin wallet on any hardware device – computer, cellphone, memory stick, external hard-drive -- and they are damaged beyond repair then your Bitcoins have been destroyed. There are certain measures that can be taken to attempt to recover the wallet but nothing is guaranteed. If you live in an area where you lose electrical power and/or Internet, cellphone connectivity then your Bitcoins are virtually destroyed since you can’t do anything with them, they are worthless which is the antithesis of a store of value.

Does a Bitcoin have diverse market utility and value? No, the only use for a Bitcoin is on the Bitcoin blockchain to transact payments. The long-run exchangeable value of a Bitcoin depends on the demand for people to use the Bitcoin blockchain to transact business. If that demand dries up so does the exchangeable value of Bitcoins.

Speculative value is not the same as exchangeable value. In other words the fact that the price of Bitcoin fluctuates wildly – it lost 80% of its price in one year and 24% in one weekend -- isn’t a characteristic of a store of value. The speculative value depends on the speculator not using, not exchanging his Bitcoins on the blockchain but rather continuing to hold them in hopes of recovering from the wild price dips and the price climbing in order to profit from continued speculative demand. A store of value must have value that can be used in exchange at any time in the long-run regardless of the price.

The Supply of Bitcoins

As with all artificial goods Bitcoin has a deterministic, perfectly inelastic supply, determined outside the market which is completely insensitive to changes in demand and price. It’s programmatically determined so that there is always a discrete number of Bitcoins created every time period. The software is written to manipulate Bitcoin “mining” rates in order to ensure a fixed number of Bitcoins are created every 10 minutes regardless how many “miners” there are. This fixed amount is halved every four years or so. It started at 50, then halved in 2012 to 25, in 2016 it halved again to 12.5 and in 2020 it halved to 6.25. The same amount of Bitcoins are deterministically created every time period regardless of the demand and price. The supply is vertical, perfectly inelastic in both the short-run and the long-run. It also means that the rate of increase of the supply of Bitcoins is decreasing over time and there’s nothing the market can do to change that.

The Demand for Bitcoins

A blockchain is a real economic good, it’s a data store that must be specified, designed, built, tested etc. just like any software engineering product. There are many commercial uses for blockchain datastores. The utility in the Bitcoin payment network is the blockchain and the fact that all transactions are mathematically related to one another making it difficult to falsify. But since you can’t trade dollars on the blockchain, a perfectly complementary artificial good—a Bitcoin—was created. The original demand for a Bitcoin came from the demand to use the blockchain as a payment system rather than other payment systems like PayPal for transacting financial payments. Being a perfect complement with no substitutes, the fundamental demand for a Bitcoin represents one’s valuation of the blockchain as a payment network and so is a downward sloping curve.

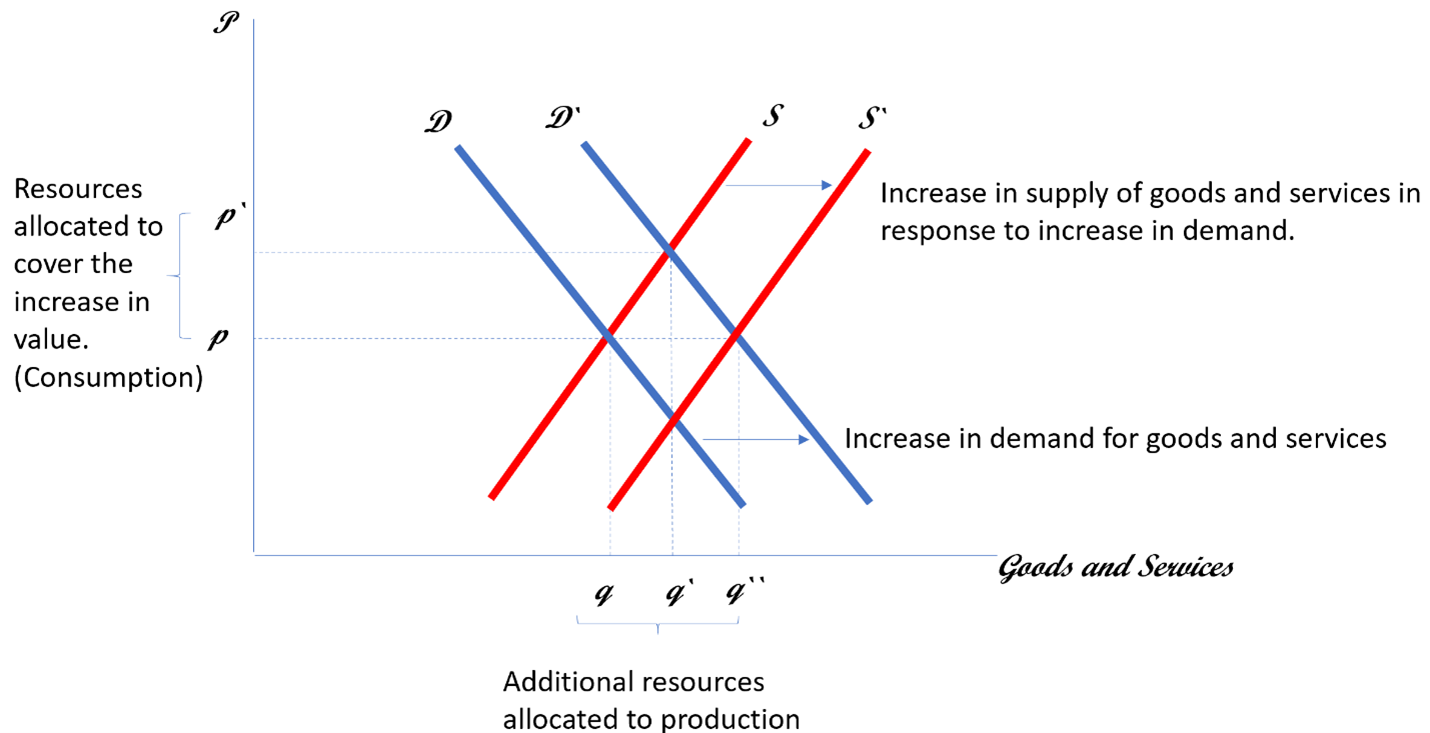

Supply, Demand and Price of a Real Economic Good

In a market, price indicates the market’s valuation of a good or service. For a real good with an upward sloping supply curve, any increase in demand will result in an increase in price in the short-run for any given level of supply. The increase in price will signal those with unemployed resources that there is potential profit to be made and those resources will be reallocated to increase production and supply in the market. In the long-run this increase in supply will bring prices back down adding a price stabilizing effect to the market.

In other words:

PriceGoods = market valuation of the good or service

Short-run

Long-run

Supply, Demand and Price of Bitcoin

Since the supply curve for Bitcoins is vertical, perfectly inelastic and determined outside the market, it does not adjust in reaction to an increase in demand and price. The supply of Bitcoin is mutually exclusive from market forces, so the same increase in demand as with a real economic good will result in only an increase in the price of Bitcoins in the short-run with no stabilizing offset in supply in the long-run. In other words the price will go up and just stay there, there is no offset in supply to stabilize it. Part of the increase in price will represent the increase in demand and the rest is a dead weight loss that doesn’t represent value but simply a cost imposed due to the artificial nature of Bitcoins.

In other words: PriceBitcoin = market valuation of Bitcoin + dead weight loss.

Therefore, PriceBitcoin > PriceGoods for the same increase in demand.

This deadweight loss incorporated into the price of Bitcoin accumulates over time reallocating productive resources to non-productive purposes. The price of Bitcoin therefore increases disproportionately to real economic goods due to its artificial nature and it’s this disproportionate increase in price relative to real economic goods that is the catalyst for speculative demand.

Consumption Demand vs. Speculative Demand

The Federal Reserve has been engaging in what it called “Quantative Easing” since 2009 and in 2020 alone it created 21% of all US Dollars in circulation. When central banks inflate the money supply, the demand for all goods increases. Since the Bitcoin payment network is used to process payments for goods and Bitcoin is a perfect complement for that network, as the demand for goods increased due to the inflation of the money supply, so did the demand for Bitcoins in order use the Bitcoin payment network to pay for them.

Key point: At the same time that the demand for real goods was increasing and driving the increase in the demand for Bitcoins, the price of Bitcoins was increasing disproportionately to the price of the goods they were paying for.

Someone with Bitcoins will see the disproportionate increases in price relative to real goods and choose to hold their Bitcoins rather than trade them for goods with disproportionately lower value. This is because they can always trade for those real goods with cash or some other payment method without having to sell their Bitcoins which are disproportionately increasing in price. Eventually, consumers will substitute alternative payment methods for the Bitcoin payment network which means they’ll hold their Bitcoins which is speculative in nature. At some point speculative demand for Bitcoins becomes greater than consumption demand.

For example: if you have $100 worth of Bitcoin and someone is selling a guitar for $100 and will accept Bitcoin for the transaction then you can pay for the guitar on the Bitcoin blockchain payment network. Then you’ll have $0 in Bitcoin but you’ll have the guitar which you value at $100. If soon after that the price of Bitcoin doubles again as it’s done in the past then you lose out on the $100 profit you could have made if you hadn’t paid for the guitar with Bitcoin. Effectively, the guitar purchase cost you $200 = $100 price + $100 lost speculative profit. It’s more profitable to just pay for the guitar with cash and hold the Bitcoin, then the speculative profit from Bitcoin pays for the guitar.

This is obvious by the disproportionate increase in the price of Bitcoin over the years (figure 1) while daily transactions on the Bitcoin blockchain have remained relatively flat (figure 2) indicating that the overwhelming demand for Bitcoins is not a consumption demand but a speculative demand. People aren’t buying them to use them they are holding them for speculative gains.

Figure 1 Bitcoin Price History

Figure 2 Daily Bitcoin Transactions

Source: Coin Desk

Manipulating Demand and Price

In order to manipulate price in the market for a real good, one would have to be able to manipulate both supply and demand which is really impossible to do in any profitable way. But given the artificial nature of Bitcoin and the perfectly deterministic supply, all one needs to do in order to manipulate the price is to manipulate demand which is much easier and done regularly in other artificial markets such as stocks and bonds.

One of the best things about a Bitcoin wallet is that anyone can have one. One of the worst things about a Bitcoin wallet is that anyone can have one, and they do. Government agencies, central banks, corporations, financial whales etc. Those with the financial resources to ‘pump’ up the demand and price and then ‘dump’ their Bitcoins for profit.

Bitcoin exchanges also engage in ‘wash transactions’ where they effectively buy and sell Bitcoins to themselves in order to artificially stimulate demand and price.

Why is the current price of a Bitcoin so high?

As mentioned, the ongoing inflation of the money supply by the Federal Reserve increases demand and causes price inflation across all markets. Bitcoin is affected by the fact that the Bitcoin payment network is used to pay for goods which increases demand and the price for Bitcoins.

But, unlike the price of real goods which have price stabilizing mechanisms on the supply side, Bitcoin is a fixed supply which is completely unaffected by increases in demand and price. So for any given level of demand, when price goes up it just stays there, it has nowhere to go, there are no market forces to bring it back down. The price continues to go up as people switch more and more of their consumption demand for all goods to a speculative demand for Bitcoin, a classic financial bubble. That coupled with the demand manipulations leads to a highly risky and volatile long-run price. The price volatility is due to the disproportionate changes in price. Just as the price goes up disproportionately to real goods, that’s the way it comes back down leading to the wild swings in price over the years.

Conclusion

Bitcoin doesn’t possess any of the economic fundamentals to be a real economic good, a store of value or a medium of exchange. The dead weight loss associated with the price of Bitcoin is economic resources being transferred from productive endeavors in order to pay a tax imposed on the price of Bitcoin due to nothing but its artificial nature.